Inverted yield curve

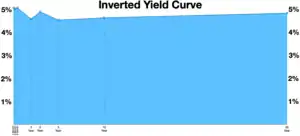

In finance, an inverted yield curve happens when a yield curve graph of (typically) government bonds inverts and the shorter term bonds are offering a higher yield than the long-term bonds. Longer maturity bonds usually have a higher percent yield return because they are more risky because of volatility in the market, there could be a liquidity trap that wouldn't allow an investor to sell the bond security on the secondary market over the long run and they could get stuck with an underperforming asset. The inverted yield curve is one of the most reliable leading indicators for economic recession since at least 1955. The US Federal Reserve uses open market operations to adjust the Federal funds rate which pushes up short term bonds to catch the longer maturity bonds which are rising to catch up to inflation during the flattening of the yield curve.[2] The inversion of the yield curve tends to predate a recession 7 to 24 months ahead of time,[3][4] but inversion during a labor shortage and low indebtedness in 2023 raised questions over whether widespread awareness of its predictive power made it less predictive.[5]

History

The term "inverted yield curve" was coined by the Canadian economist Campbell Harvey in his 1986 PhD thesis at Duke University.[6]

Business cycles

The inverted yield curve is the contraction phase in the business cycle or credit cycle when the federal funds rate and Treasury interest rates are high to create a hard or soft landing in the cycle. When the Federal funds rate and interest rates are lowered after the economic contraction (to get price and commodity stabilization) this is the growth and expansion phase in the business cycle. The Federal Reserve only indirectly controls the money supply and it is the banks themselves that create new money by fractional-reserve banking when they make loans. By manipulating interest rates with the Federal funds rate and repurchase agreement (repo market) the Fed tries to control how much new money banks create.[7][8]

Other countries bond yields that have inverted

German bonds Inverted yield curve in 2008 and Negative interest rates 2014-2022

30 year

10 year

2 year

1 year

3 month

|

United Kingdom bonds

50 year

20 year

10 year

2 year

1 year

3 month

1 month

|

Canada bonds

30 year

10 year

2 year

1 year

3 month

1 month

|

Portugal bonds during European sovereign debt crisis

30 year bond

10 year bond

5 year bond

1 year bond

3 month bond

|

Ireland bond prices, Inverted yield curve in 2011 during European debt crisis and Ireland banking crisis[9] And rates went negative after the European debt crisis

15 year bond

10 year bond

5 year bond

3 year bond

|

Russian bonds, Inverted yield curves to tame inflation during their wars (Russo-Georgian War, Russo-Ukrainian War, 2022 Russian invasion of Ukraine)

20 year bond

10 year bond

1 year bond

3 month bond

|

Sri Lanka bonds spiked in 2022 Inverted yield curve in the first half of 2022 during Sri Lankan economic crisis 15 year bonds

10 year bonds

5 year bonds

1 year bonds

6 month bonds

|

Brazilian bonds had an Inverted yield curve starting in August 2014 as part of the 2014 Brazilian economic crisis

10 year bond

5 year bond

1 year bond

|

Iceland bonds had an Inverted yield curve in 2008 during the 2008–2011 Icelandic financial crisis

10 year bonds

5 year bonds

2 year bonds

|

Japan bonds Inverted yield curve in 1990 Zero interest-rate policy starting in 1995 Negative interest rate policy started in 2014 30 year

20 year

10 year

5 year

2 year

1 year

|

New Zealand bonds Inverted yield curve in 1994-1998 and 2004-2008 20 year

10 year

2 year

3 month

1 month

|

Yield spreads

Yield spread is the difference between the quoted rates of return on two different investments and for the inverted yield curve it is United States Treasury Bonds. It is simply done by subtracting the percent yield on one bond vs another bond of a different duration. For example a 30 year bond with a 6% yield minus a 2 year bond with a 4% yield would be a spread of 2% or 200 basis points. Another example would be a longer duration bond of 10 years at 3% minus a shorter duration bond of 3 months at 3.5% would be -0.5% or a negative yield spread. [10]

See also

References

- "US Treasurys". CNBC. September 25, 2012.

- "Flat Yield Curve". Investopedia.com.

- "What Is an Inverted Yield Curve?". Investopedia.com.

- Bruce-Lockhart, Chelsea; Lewis, Emma; Stubbington, Tommy. "An inverted yield curve: why investors are watching closely". Ig.ft.com.

- Darian Woods; Adrian Ma (April 14, 2023). "An indicator that often points to recession could be giving a false signal this time". All Things Considered.

- Campbell R. Harvey. "Yield Curve Inversions and Future Economic Growth" (PDF). Faculty.fuqua.duke.edu. Retrieved 26 July 2022.

- "Here We Go Again: The Fed Is Causing Another Recession". Mises Institute. June 21, 2022.

- "Reference Rates - FEDERAL RESERVE BANK of NEW YORK". Newyorkfed.org.

- https://www.researchgate.net/figure/a-Irish-yield-curve-dynamics-around-2011-loan-amendments-b-Portuguese-yield-curve_fig2_342609297

- "Yield Spread Definition".